The cleantech, tech, stock, and business news of this past week was more obvious than an elephant sitting in a Fiat 500e — Elon Musk may take Tesla private.

It has stunned the world, and the response from the financial press has been embarrassing — to put it nicely.

One matter very frequently ignored is what an exclusive share in private Tesla should actually be worth. This is different from what a share in public TSLA is worth right now or should be worth right now. Investors — especially small fries like me and most of you — probably won’t even have the opportunity to acquire Tesla shares again until Tesla goes for another IPO (presuming that does happen again).

So, always eager to put myself out on a thin limb that is almost certain to break, I wanted to run through a rough “back of the envelope” estimate of what Tesla might be worth in 5–10 years when it hypothetically rejoins public markets (… which it hasn’t actually left yet). One thing to remember with this speculation, of course, is that there’s no magic formula for determining a company’s value. There are all kinds of different quantitative and qualitative ways to value a company, but since so many people use so many different mixtures, the end result is generally unpredictable.

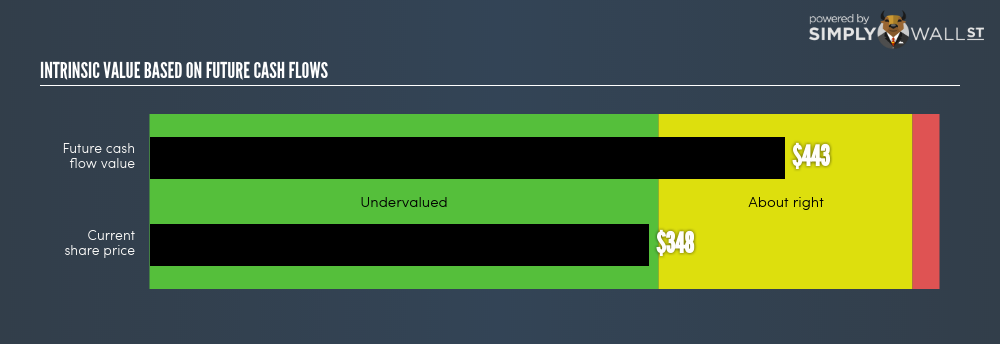

But let’s start with today. “Artful Dodger” writes, “The simplywall.st website calculates the intrinsic value of every stock on NASDAQ each night, based on estimated 5-year discounted cash flows. Their number on Aug 3rd, after the Q2 ER, but before Elon’s tweet, was $443 per share. Unchanged today. It was $421 before the Q2 ER.”

Yep, that simple and common analysis puts Tesla’s “intrinsic value” share price at $443 — or something around that number. That means $420 is in the right range but actually on the lower end of the range. Additionally, remember, this is for a public company that’s expected to stay public — not a public company on the verge of going private for an indefinite period of time.

At the end of 2017, I played with some Tesla numbers and came up with an estimate of $73.7 billion in Tesla vehicle revenue in 2022 — probably a bit optimistic (“Elon time”) on the timeline since I assumed Model Y would be at full production (700K/year) by then. But let’s just assume a slight variation of these are the numbers we see when Tesla feels comfortable re-emerging for another go at an IPO.

| Vehicle | Orders | Average Price | Total Revenue | Profits based on 20% Gross Margin | Profits based on 25% Gross Margin |

| Tesla Semi | 47,000 | $200,000 | $9,400,000,000 | $1,880,000,000 | $2,350,000,000 |

| Tesla Model 3 | 400,000 | $42,000 | $16,800,000,000 | $3,360,000,000 | $4,200,000,000 |

| Tesla Model S | 45,000 | $84,000 | $3,780,000,000 | $756,000,000 | $945,000,000 |

| Tesla Model X | 55,000 | $91,000 | $5,005,000,000 | $1,001,000,000 | $1,251,250,000 |

| Tesla Model Y | 700,000 | $50,000 | $35,000,000,000 | $7,000,000,000 | $8,750,000,000 |

| Tesla Pickup | 55,000 | $63,000 | $3,465,000,000 | $693,000,000 | $866,250,000 |

| Tesla Roadster 2 | 1,100 | $230,000 | $253,000,000 | $50,600,000 | $63,250,000 |

| TOTAL | 1,303,100 | $73,703,000,000 | $14,740,600,000 | $18,425,750,000 |

In that scenario, some of the biggest wildcards in terms of annual production and sales were: 47,000 Tesla Semis, 55,000 Tesla Pickups, and 700,000 Tesla Model Ys. I later created what I think is a more realistic estimate of 100,000 Semis per year. Throwing in some rough gross margin estimates, that put profits from the Semi at $3–5 billion a year instead of ~$2 billion a year.

Anyway, it’s all a guessing game, so why don’t we stick with my initial estimate of $14.7 billion in annual vehicle profits. And maybe throw in another $5 billion for Tesla Energy products. At that point, what’s the company “worth?” $100 billion? $200 billion? The latter makes the company approximately 3.3 times more valuable than it is today. Multiplying $360 by 3.3, I land on $1190. Multiplying $443 by 3.3, I land on $1460. I think that’s getting close to the value I see some Tesla investors putting on a share of a private Tesla. Others are looking further out and have double that in mind, if not more.

Furthermore, there are entire business avenues we’ve ignored — a potential Tesla network for on-demand robotaxi service, minibuses, microcars, etc. Taking all of these into account, how much should $1190 or $1460 be increased?

Some Tesla shareholders happy to go private with their shares are dreaming of a 10× increase in value before the company IPOs again, something that would mean $3600 a share today or $4430 at the “proper” price. That would put the company’s value at $600 billion, which is still conservative if you believe Elon Musk’s forecast that Tesla could become as valuable as Apple by 2025 — something the likes of Ron Baron and Gene Munster might agree with. By the way, that 2015 forecast from Elon Musk was when Apple had just passed $700 billion in value. More recently, Apple became the first public company to skate past $1 trillion in value.

But where will Tesla really be when it holds another IPO? Nobody has a clue. Elon Musk isn’t even certain there would be another IPO, but that seems to be the expectation.

Furthermore, the company will regularly get valued off the public market as well. How quickly will that value grow with Tesla unhindered by short sellers, fear-mongering press reports, and misleading claim after misleading claim about “cash burn” or “impossible” production targets?

To repeat it for the 5th time or so: There are numerous ways to value a private company, and even for public companies, target valuations from various expert analysts are all over the map. In Tesla’s case, they are hundreds of dollars per share apart today between the low bear forecasts and the high bull forecasts. For anyone planning to hold onto Tesla shares until it comes out for another IPO (through a long period of being private), the mystery is how the market will value it if you presume production is running at full speed at multiple gigafactories and delivering over a million units combined of the Model 3, Model Y, Model S, Model X, Semi, Pickup, and Roadster each year — not to mention various energy products and surely something new. Throw in a Tesla Network or two for double the speculation, double the fun.

I think you get the point. It’s a WAG judgement call on what Tesla will do once private, what it will achieve, and how its value will change off the public market and perhaps back on it in the next 10 years. Going on the last 10 years, a lot of us have high expectations and can’t think of a better company to put our money into. Nonetheless, certainly don’t take that as investment advice. Actually, just take that cash and put it into a CleanTechnica membership or ambassadorship.

Avots: cleantechnica

{kind=link}